尊敬的用戶您好,這是來自FT中文網的溫馨提示:如您對更多FT中文網的內容感興趣,請在蘋果應用商店或谷歌應用市場搜尋「FT中文網」,下載FT中文網的官方應用。

Exchange traded fund investors pumped record sums into fixed income and “quality” stocks last year as risk appetite jumped in the final months of 2023.

隨著風險偏好在2023年最後幾個月躍升,交易所交易基金投資者去年向固定收益和「優質」股票注入了創紀錄的資金。

However inflation-linked bond funds and broad commodity ETFs experienced record outflows as sliding global inflation tempered investors’ desire to hedge against its corrosive effect on asset prices.

然而,與通膨掛鉤的債券基金和大宗商品ETF卻經歷了創紀錄的資金流出,原因是全球通膨下滑削弱了投資者對沖通膨對資產價格腐蝕性影響的願望。

Overall, the global ETF industry recorded net inflows of $965bn last year, according to data from BlackRock, up from $867bn in 2022. This was the second-highest figure on record, behind 2021’s $1.3tn.

貝萊德的數據顯示,去年全球ETF行業總體錄得9650億美元的淨流入,高於2022年的8670億美元。這是有史以來第二高的數字,僅次於2021年的1.3兆美元。

“It’s interesting to see it compare to 2021, even though we had so many rate hikes,” said Karim Chedid, head of investment strategy for BlackRock’s iShares arm in the Emea region, referring to the fact that tighter monetary policy tends to weigh on equity and bond prices.

貝萊德旗下安碩(iShares)在歐洲、中東和非洲地區的投資策略主管卡里姆•切迪德(Karim Chedid)表示:「與2021年相比這很有趣,儘管我們有那麼多次加息。」他指的是貨幣政策收緊往往會給股票和債券價格帶來壓力。

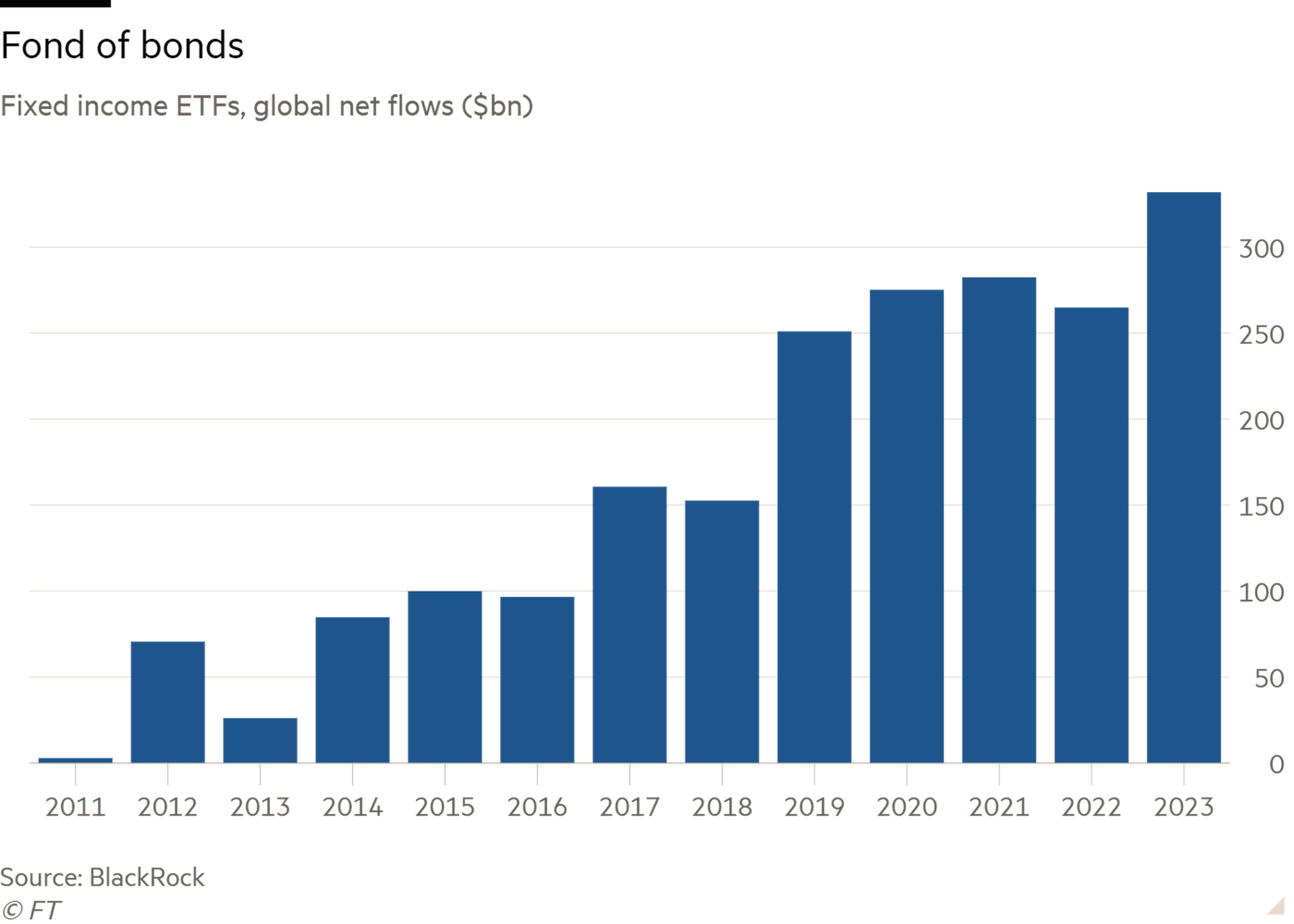

Unlike 2021 and 2022, when equity funds dominated, ETF flows were more balanced last year. Stock funds sucked in a net $640bn, below the $1tn of 2021, but fixed income ETFs vacuumed up a record $332bn, surpassing the previous zenith of $282bn in 2021.

與股票基金占主導地位的2021年和2022年不同,去年ETF的資金流動更爲平衡。股票基金淨吸納6400億美元,低於2021年的1兆美元,但固定收益ETF吸納了創紀錄的3320億美元,超過了2021年2820億美元的上一個頂峯。

Fixed income’s record year was capped by a sharp pick-up in risk appetite in the final quarter. Flows into sovereign bond ETFs, which had dominated earlier in the year, fell to $31.9bn in Q4, their lowest figure since Q1 2022.

最後一個季度,風險偏好急劇上升,爲固定收益創紀錄的一年畫上了句號。今年早些時候占主導地位的主權債券ETF流入量在第四季度降至319億美元,爲2022年第一季度以來的最低水準。

However riskier corporate bond flows spiked to $29.1bn in the quarter. The volte-face was particularly notable in high-yield bonds, which saw year-to-date net outflows of $8bn as of October 27, but then took in $17.1bn in the remainder of 2023.

然而,風險較高的公司債流動飆在本季度升至291億美元。這種大轉變在高收益債券領域尤爲明顯,截至10月27日,當年淨流出80億美元,但隨後在2023年剩餘時間裏流入171億美元。

Chedid said investors were “locking in higher yields” before they started to slide in line with inflation and interest rate expectations.

切迪表示,在收益率開始隨著通膨和利率預期下滑之前,投資者「鎖定了更高的收益率」。

Todd Rosenbluth, head of research at VettaFi, a consultancy, saw the scope for more buying to come.

諮詢公司VettaFi的研究主管託德•羅森布魯斯(Todd Rosenbluth)認爲,未來還會有更多的買盤。

“We are still in the early stages of fixed income [ETF] adoption globally,” he said. “Investors embraced fixed income ETFs in a rising rate environment and returns are likely to be better in 2024 if, as expected, the US Federal Reserve begins and continues to cut interest rates.”

「我們仍處於全球採用固定收益ETF的早期階段,」他表示。「投資者在利率上升的環境中接受了固定收益ETF,如果美聯準像預期的那樣開始並繼續降息,2024年的回報率可能會更好。」

The “everything rally” in the fourth quarter also bolstered equity ETFs. Those focused on US equities enjoyed their highest inflows on record in the fourth quarter, $197bn, helped by December’s record monthly tally of $97.2bn. Higher-risk emerging market equity ETFs saw their third-best month ever, taking in $22.3bn, the BlackRock data show.

去年第四季度的「全線反彈」也提振了股票型ETF。在去年12月創紀錄的972億美元的月度流入的推動下,專注於美國股市的ETF在第四季度獲得了創紀錄的1970億美元資金流入。貝萊德的數據顯示,風險較高的新興市場股票ETF出現了有史以來第三高的月度表現,共募集資金223億美元。

Sector-wise, 2023 was all about technology ETFs, which garnered $52.2bn, a light year away from the second most popular sector, financials, with $3.8bn.

從板塊來看,2023年科技股ETF大行其道,共吸金522億美元,第二大熱門板塊金融類的38億美元與之相比差距巨大。

In terms of investment “factors”, quality — stocks with a high return on equity, stable earnings growth and low leverage — ruled the roost, with a record $36bn of net buying.

在投資「要素」方面,優質股票——股本回報率高、盈利成長穩定、槓桿率低的股票——佔據主導地位,淨買入額達到創紀錄的360億美元。

As a result, the iShares MSCI USA Quality Factor ETF (QUAL) was in the top 10 of US-listed ETFs by flows last year, with $11.1bn, Rosenbluth said, as quality stocks “did well in an uncertain economic environment”. QUAL returned 30.9 per cent last year, beating the S&P 500 by 4.6 percentage points.

羅森布魯斯表示,其結果是,iShares MSCI USA Quality Factor ETF (QUAL)去年以111億美元的資金流躋身美國上市ETF的前十名,因爲優質股票「在不確定的經濟環境中表現良好」。QUAL去年的回報率爲30.9%,比標準普爾500指數高出4.6個百分點。

Funds targeting cheaper “value” stocks amassed just $5.3bn, the lowest reading for four years, while minimum volatility ETFs bled $16.4bn.

瞄準價格較低的「價值型」股票的基金僅募集了53億美元,爲4年來的最低水準,而波動性最低的ETF則流失了164億美元。

ETFs investing on the basis of environmental, social and governance concerns also drifted out of favour. Even in their European heartland, they only accounted for 29 per cent of ETF inflows last year, compared with 61 per cent in 2022, according to Invesco.

基於環境、社會和治理問題進行投資的ETF也逐漸失寵。根據景順(Invesco)的數據,即便是在歐洲中心地帶,去年它們也只佔ETF流入量的29%,而2022年這一比例爲61%。

Also in the doghouse were inflation-linked bond ETFs, which haemorrhaged a record $20.7bn, as waning inflation eroded their appeal.

與通膨掛鉤的債券ETF也受到冷落,損失了創紀錄的207億美元,原因是通膨減弱削弱了它們的吸引力。

The iShares TIPS Bond ETF (TIP) alone shipped $4.5bn, Rosenbluth said, as investors “were less apt to protect against an inflationary environment in 2023”.

羅森布魯斯表示,僅iShares TIPS Bond ETF (TIP)就流出了45億美元,因爲投資者「不太願意防範2023年的通膨環境」。

Slowing inflation may also have been a factor in the continued travails of commodity exchange traded products, which lost $15.4bn, their third straight year of outflows. Gold funds accounted for the bulk of this, shipping $13.5bn, the second-worst tally ever, while broad commodity vehicles shed $3bn, an all-time high.

通膨放緩也可能是大宗商品交易所交易產品持續虧損的一個因素,它們損失了154億美元,爲連續第三年流出。其中,黃金基金佔了大部分,流出135億美元,爲有史以來第二差,而廣義大宗商品基金則流出30億美元,創歷史新高。

“Given gold’s positive performance, this trend of under-allocating could be considered a missed opportunity by ETF investors,” said Matthew Bartolini, head of SPDR Americas research at State Street Global Advisors.

道富環球投資管理SPDR美洲研究主管馬修•巴托里尼說:「鑑於黃金的積極表現,這種低配趨勢可能會被ETF投資者視爲錯失良機。」

Chedid compared gold to value stocks, in that both tended to draw money during inflationary periods, but was nevertheless surprised by the unpopularity of gold ETPs, given the price rose 13 per cent last year. “The correlation between the two has broken down,” he said.

切迪將黃金與價值型股票進行了比較,因爲兩者都傾向於在通膨時期吸引資金,但他還是對黃金ETF不受歡迎感到意外,因爲金價去年上漲了13%。他說:「兩者之間的相關性已經被打破了。」

Chedid saw reasons to believe the bullish environment could continue into 2024.

切迪有理由相信,看漲的環境可能會持續到2024年。

“The risk rally has further legs to go if you consider there is a lot of cash on the sidelines that can be deployed,” he said, with safety-first money market funds attracting nearly $2tn last year, pushing their assets to $8tn, while in Europe average cash allocations in wealth portfolios have risen from 3 per cent in 2021 to 8 per cent.

他表示:「如果你考慮到有大量可以配置的場外現金,那麼風險上漲還有進一步的空間。」以安全爲優先的貨幣市場基金去年吸引了近2兆美元資金,使其資產規模增至8兆美元,而在歐洲,財富投資組合中的平均現金配置比例已從2021年的3%升至8%。

Rosenbluth was also upbeat, but expected a stock rotation. “I do think we are going to see great demand and strong performance for value investing. [These stocks] tend to do better in a falling interest rate environment. Financials, consumer staples and energy are favoured in value strategies,” he said.

羅森布魯斯也表示樂觀,但預計會出現股票輪動。他說:「我確實認爲我們將看到價值投資的巨大需求和強勁表現。[這些股票]在利率下降的環境中往往表現更好。在價值投資策略中,金融股、主要消費品和能源股受到青睞。」

However Chedid warned that BlackRock’s house view is that the six interest cuts priced in for the US this year are “excessive”.

然而,切迪警告稱,貝萊德的觀點是,市場對美國今年6次降息的預期是「過度的」。

“We are not in the camp that inflation will come down nicely. Labour supply is tight in the US,” he said.

他說:「我們並不認爲通膨會很好地下降。美國的勞動力供應緊張。」

More broadly, “from a macro perspective it’s hard to argue that there won’t be any volatility this year,” which central banks may be unable to help out with, unlike in the days of quantitative easing.

更廣泛地說,「從宏觀角度來看,很難說今年不會有任何波動」,與量化寬鬆時期不同,央行可能無法幫助解決這些波動。

“That’s the headwind for the risk rally that we saw in Q4,” Chedid said.

「這是我們在第四季看到的風險反彈的逆風,」 切迪表示。

Bartolini shared these concerns. “US equity markets, the engine behind the surge in global stock returns, enter 2024 with stretched valuations,” he said. “And geopolitical risks are likely to intensify, given 76 countries will hold elections in 2024.”

巴托里尼也有同樣的擔憂。他表示:「作爲全球股市回報飆升背後的引擎,美國股市在進入2024年時估值過高。考慮到2024年將有76個國家舉行選舉,地緣政治風險可能會加劇。」